Pass-Through Entities Claiming the Employee Retention Credit May Have a Limited 199A Deduction

Careful analysis of the employee retention credit (“ERC”) provided under the Coronavirus Aid, Relief, and Economic Security Act (“CARES Act”) and the 199A limitations set forth under the Tax Cuts and Jobs Act of 2017 (“TCJA”) may lead to unexpected tax consequences this tax season. Just when we thought the discussion surrounding 199A was on the decline, the detailed review of the IRC and regulations could limit the 199A deduction for certain pass-through entity owners, causing their effective federal tax rate to jump from 30% to 37%.

As you may recall, the 199A deduction was incorporated in the TCJA as a compromise for pass-through entities owners after significant public comment following the proposed decline of the corporate tax rate 35% to 21%. After all, why were the large C Corporations being given such favorable treatment when the majority of the businesses in the United States operate as pass-through entities? While the government would not give pass-through entity owners a direct tax rate decrease, they created a fictitious deduction of up to 20% related to pass-through business income provided certain conditions were met. The 199A deduction can potentially allow pass-through entity owners a decrease in their federal effective tax rate from 37% to approximately 30%. In a simple example, if a taxpayer received pass-through entity business income of $100,000, the 199A deduction could be up to $20,000. If the $100,000 was subject to an effective tax rate of 37%, with no 199A deduction, the tax due would be $37,000. However, because a fictious deduction is allowed, the taxable income subject to 37% would decrease to $80,000 (100,000-20,000 199A deduction) and result in tax due of 29,600, or an effective tax rate of 29.6% (29,600/100,000).

Several requirements must be met in order to take the 199A deduction, including the requirement that the related activities give rise to an active trade or business. However, the 199A rules become even more complicated in instances where a taxpayer’s taxable income exceeds certain threshold amounts. If a single taxpayer’s 2021 taxable income exceeds $214,900, or $429,800 for a married filing joint taxpayer, additional definitions and limitations are evaluated. For example, if the pass-through entity is considered to be a specified service trade or business, often referred to as an SSTB, no 199A deduction is allowed. SSTBs include businesses providing services in the field of health, law, accounting, actuarial science, performing arts, athletics, and financial services.

Provided that the pass-through entity income is not considered to be related to a SSTB, and the taxable income of the taxpayer exceeds the stated amounts, then the amount of 199A deduction is limited to the greater of:

- 50% of W-2 wages with respect to the qualified trade or business or

- 25% of W-2 wages plus 2.5% of the unadjusted basis of qualified property

If a taxpayer is not conducting an SSTB and their taxable income exceeds the 199A thresholds, the question of whether W-2 wages can include wages that were utilized to calculate the employee retention credit becomes extremely important. The employee retention credit could impact the 199A deduction for a significant number of pass-through entities that have little to no qualified property, including many in the service industry.

Example: ERC Reduction in 199A Wage Limitation

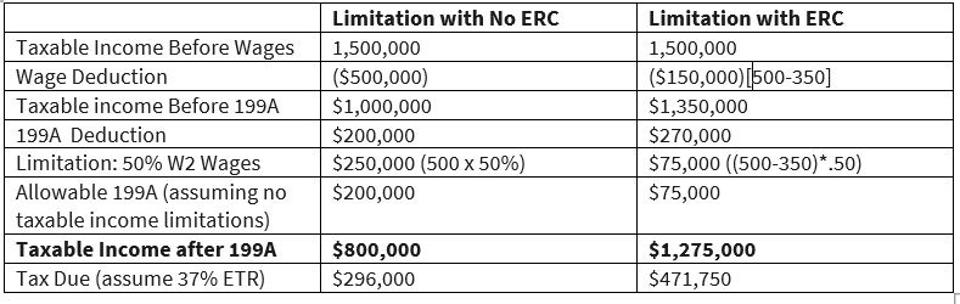

Before walking through the technical law, let’s review a basic example to measure the potential impact. Assume that an S Corporation has a sole shareholder who operates a restaurant for the 2021 tax year and paid salaries and wages of $500,000 and has zero qualified property. Let’s also assume that the employer qualified for the employee retention credit and calculated a 2021 employee retention credit of $350,000. Lastly, the taxable income before salaries and wages is $1,500,000.

While many are familiar with the fact that the salaries and wages deduction must be decreased by the amount of the employee retention credit claimed for the taxable year when calculating taxable income, the W-2 wages used for the 199A wage limitation must also be reduced.

The impact that the ERC has on the 2021 taxable income calculation would be as follows:

When comparing the fact pattern above, taxable income when claiming the employee retention credit is increased by not only the $350,000 of disallowed salary deduction, but also another $125,000 due to the diminished W-2 wages being allowed for purposes of the 199A wage limitation. In other words, the total cash received of $350,000 for the ERC is being reduced by additional taxes of $175,750 (475,000 x 37%) for a cash benefit remaining after taxes of only $174,250 (350,000-175,750).

While some people might argue that the S corporation shareholder still realizes a positive cash impact, the limitation and tax impact of the ERC for pass-through entities is inconsistent when compared to C corporations. In the same example above, if the entity were considered a C Corporation, the taxable income would be $1,350,000 with a tax due amount of $283,500 (1,350,000 x 21%). This would result in a current year tax cash due related to the employee retention credit of $276,500 ($350,000 – (350,000 x 21%) for the C Corporation, compared to a cash impact of only $174,250 for the pass-through entity in our example. This results in over $100,000 more cash for the C corporation. In other words, the 21% corporate tax rate has no dependency on the amount of taxable income being generated or the underlying wages or qualified property in the business. While we can’t ignore the double taxation for C corporation earnings when also considering shareholder distributions, the ability to control the timing of that second layer of taxation is beneficial.

The impact of the ERC wage limitation could potentially be limited if there are other pass-through entities where 199A aggregation could be elected. Careful review and consideration should be conducted to determine if additional aggregation can occur under the specific rules provided under Treasury Regulation 1.199A-4(c). It should be noted that once an aggregation election is made it must be followed in all subsequent year unless a significant change in facts and circumstances occurs.

Technical Law Analysis

In order to come to the conclusion that the 199A wage limitation is reduced by any employee retention credit claimed, you must follow the bouncing ball throughout the Internal Revenue Code.

The W-2 wages are defined under 199A(b)(4) to include remuneration for services performed by an employee for his employer. At the most basic definition, the wages that were paid to employees during the year, regardless of whether they were utilized for purposes of the employee retention credit, would be included. However, the definition of wages continues to state that the amount cannot include any amount which is not properly allocable to qualified business income. Qualified business income includes the net amount ofqualified items of income, gain, deduction and loss with respect to any qualified trade or business of the taxpayer. Theterm qualified items of income, gain, deduction, and loss includes items of deduction, but only to the extent such items are allowed in determining taxable income. And there is the rub.

Section 2301(e) of the CARES act provides that the rules of section IRC 280C(a) should also apply to the employee retention credit. IRC Section 280C(a) specifically states that no deduction is allowed for the portion of wages or salaries paid or incurred for the taxable year which are equal to the sum of the credits taken. In other words, not only does the employee retention credit reduce the amount of salaries and wages when determining taxable income, but because the salaries and wages were not allowed when determining taxable income, they will not be deemed properly allocable to qualified business income and therefore excluded from the definition of W-2 wages for purposes of the 199A limitation.

Does your head hurt? Mine too. I think many tax professionals have been bogged down with the ERC and the calculation of taxable income in general, and as a result, the extra step to evaluate the potential impact on the 199A wage limitation might have been on the back burner.

So what does it all mean? Evaluation of amended 2020 tax returns that already adjusted the salary and wage deduction for the ERC when calculating taxable income will need be reviewed if the W-2 199A wage limitation is pertinent. This also would impact the reporting of the W-2 199A wage limitation in 2021 if an ERC was claimed in the tax year. Lastly, estimated tax payments made with a valid extension might be larger than originally anticipated for individual pass-through entity owners.

The good news? If a taxpayer did not claim the ERC, they could have stopped reading a long time ago. If a taxpayer is under the 199A taxable income threshold amounts and claimed the ERC, all of this is inapplicable. Even if taxpayers are over the 199A taxable income threshold amounts, but are conducting an SSTB, the ERC impact on 199A W-2 wage limitation is not relevant. For everyone else, it is time to sharpen your pencils and start estimating potential impact. This is especially true for businesses with small or no qualified business property who claimed a significant amount of their salary and wage expense for the ERC. Aren’t federal income taxes grand?

This article was originally published by Lynn Mucenski Keck in Forbes on March 14, 2022.