How the IRS Is Looking for Its Share of Cryptocurrency and NFT Growth

Let’s be honest. Most tax accountants would not be described as “hip” and many struggle to be considered “tech savvy”. Even so, some of their clients’ needs are forcing them into a new world surrounding the exchange of digital assets.

While many persons trading cryptocurrency or buying a non-fungible token (“NFT”) think they are just doing something new, fun, or just goofing around because they have cash to play with, what they don’t realize is that Uncle Sam is looking to collect their share. The number of questions being asked in this space have skyrocketed. Countless persons are looking for help and are shocked when they learn of their potential tax bills. The lack of understanding and proper planning in this space can result in a significant check being made out to the IRS.

If you are one of those persons that is thinking, not again, this is just a fad, it might be time to rethink that attitude. The Crypto market capitalization, calculated by multiplying price of the cryptocurrency with the number of coins in circulation, went over $1 trillion in 2021. A large portion of the market capitalization relates to the nonfungible token (“NFT”) market. NFT sales volume totaled $24.9 billion, of which $4.8 billion was related to NFT gaming. For perspective, Crypto market capitalization in 2020 was $758 billion and the total sales in the NFT market in 2020 was just $340 million.

But is the IRS really watching this?The short answer is yes.As early as 2016, the IRS utilized a “John Doe” summons to Coinbase, which is a secure online platform for buying, selling, transferring, and storing cryptocurrency.The summons requested transaction activity for Coinbase users from 2013 through 2015 who were US persons.Coinbase was required to provide user information who bought, sold, sent or received cryptocurrency of at least $20,000 in value in one year.Based off the information received, the IRS sent 10,000 compliance letters to taxpayers advising them of their failure to properly report cryptocurrency transactions. In 2021, the IRS issued John Doe Summons to Payward Ventures (aka Kraken) and Internet Financial (Circle) seeking similar information for taxable years 2016 through 2020.In March of 2021 the IRS launched Operation Hidden Treasure, an enforcement initiative for tax violations related to cryptocurrency.And maybe you haven’t notice, but there has been a question on the individual income tax return since 2019 regarding this topic, which for 2021 asks “At any time during 2021, did you receive, sell, exchange, or otherwise dispose of any financial interest in any virtual currency?”.So if your client says the IRS will never track their virtual currency activity, think again.

Tax professionals are not only battling the murky guidance issued by the Internal Revenue Service in this space but also struggle to understand what all the terminology means when dealing with digital assets. It is the merging of two worlds: the young CPAs who are just starting to learn about tax law but are more likely to trade virtual currency and purchase NFT’s, coupled with the dinosaur CPA who thinks a hard fork is something you eat with.You get the point. The first step in minimizing unnecessary tax burdens in the digital asset space is to understand the basics surrounding virtual currency and NFT’s.

Virtual Currency

Virtual currency is a digital representation of value that functions as a medium of exchange.Cryptocurrency is a type of virtual currency that uses a blockchain to validate and secure transactions.Blockchain is a system of recording information in a way that makes it difficult or impossible to change.A blockchain is essentially a digital general ledger of transactions that is duplicated and distributed across the entire network of computers systems on the blockchain.Why do they need to use a blockchain?Because there is no regulation by a Federal Reserve board over these transactions.Instead, the community uses validation and consensus to ensure that transactions are legal and determine the ordering of events.The ability to perform validation and consensus is done by miners, requiring energy to run the machines and the ability to understand algorithms.In late 2021 the United States became the number one destination for bitcoin miners, eclipsing China for the first time in history.

But the vast majority of people involved in virtual currency are not miners.Instead, most people involved are purchasing cryptocurrency, such as Bitcoin, Ethereum, Tether, Cardano.And I can guarantee that you have some clients who are involved in cryptocurrency.And ignoring their investment or not asking the right questions is not the answer.

Every cryptocurrency is unique.But for discussion, let’s focus on the two most popular cryptocurrencies, Bitcoin and Ethereum, to explore the differences.Bitcoin, BTC, is the original cryptocurrency and runs on blockchain.Bitcoin supply will never exceed 21 million coins.It is expected that the creation of new Bitcoin will be very unlikely after 2040.

Ethereum is also a cryptocurrency but does not have an overall limit of coins to be disbursed. Ethereum does limit the yearly disbursement to 18 million.One would think the fact that the supply is not finite would mean that the value would be much less.So what makes Ethereum so special?Ethereum has a blockchain platform.This means that individuals not only can use Ethereum for investment, but with a blockchain platform they can also create Smart Contracts.Smart Contracts can automatically execute a transaction when prescribed conditions are met. Smart Contracts have been used in business cases, such as supply chain management, insurance claims, clinical trials, escrows, mortgage systems – the list goes on and on.However, the most popular use of a Ethereum’s Smart Contract is the creation of NFT’s.

So what are the basic tax consequences of receiving cryptocurrency? The first comments by the IRS in this space came throughNotice 2014-21, where they acknowledge the use of virtual currency. The IRS clearly states that for federal tax purposes, virtual currency is treated as property. The IRS also provided that general tax principles applicable to property transactions should also apply to virtual currency.So when your client tells you they acquired some Ethereum, think of it as though they bought property.

After your client tells you they have a cryptocurrency, the next question should be as to how they acquired it. The initial purchase of cryptocurrency with US dollars will not trigger income or gain for a taxpayer, and the IRS clarified in March of 2021 that if you purchased cryptocurrency using USD you do not have to check “yes” to the virtual currency question on your individual tax return.However, if your client received cryptocurrency as payment for goods or services or mines virtual currency, they will be required to include the fair market value of the virtual currency on the date of receipt in their gross income and potential self-employment tax may be required.

So my client owns virtual currency, now what? They can use their virtual currency for a variety of transactions.Some might be new to the space and just be holding the cryptocurrency as an investment. Others might exchange their cryptocurrency for other cryptocurrency when they have a hot lead or a good tip. Some use virtual currencies for everyday transactions to pay for goods or services.After all Starbucks, Home Depot, Overstock and Microsoft are all accepting some form of cryptocurrency.Your client could also use their virtual currency to buy digital artwork through an NFT of start playing NFT video games.

The IRS issuedFAQ’s for Virtual Currency, which reaffirms the IRS’s view that the disposition of virtual currency is a disposition of property and whether or not the virtual currency is sold for real currency, or exchanged for other property (including goods or services or another virtual currency), a capital gain or loss must be reported.Many virtual currency holders overlook this concept. An exchange of one virtual currency for another, a crypto-to-crypto exchange, is considered a taxable event.

A taxpayer that disposes of virtual currency will recognize a capital gain or loss that is either short-term or long-term depending on the holding period of the virtual currency disposed. The gain recognized is determined by subtracting the basis of the virtual currency being exchanged from the amount realized. The amount realized in the exchange is either the USD received, or the fair market value of the property received.The basis is the amount the taxpayer originally paid for the virtual currency.

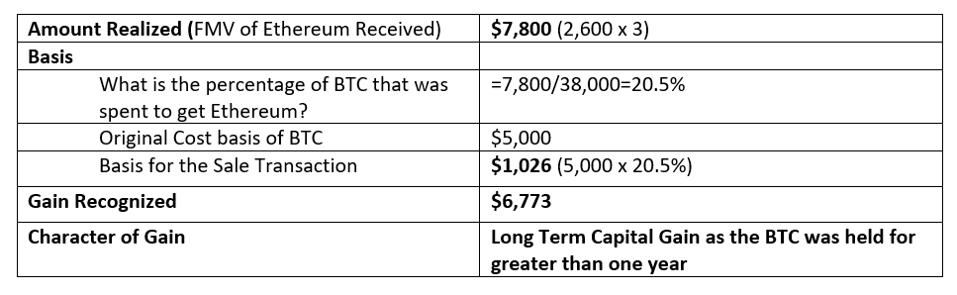

Let’s assume that Tim purchased 1 Bitcoin in March of 2020 for $5,000. In January of 2022, the Bitcoin is worth $38,000. Tim decides to exchange a fraction of his Bitcoin to invest in Ethereum.A token of Ethereum is currently valued at $2,600 and Tim purchases 3.Under the IRS guidance, the gain would be calculated as follows:

While you may view this as a simple transaction, there are basic planning strategies to minimize cash tax impact. The first point to make your clients aware of is that they should aim to hold onto the digital currency for greater than one year for more favorable tax treatment.Any gain triggered related to digital currency held longer than one year would be taxed at the long-term capital gain rate, subject to a maximum tax of 20% versus a short-term capital gain rate where the individual maximum tax rate is 37%.In our previous example, that would change the tax due from $1,354 on a long-term capital gain versus $2,506 if it was treated as a short-term capital gain.

Where many tax accountants get confused is how to calculate the basis and holding period of the virtual currency if more than one is owned.Do they use the First in First Out (FIFO), Last in First Out (LIFO), or highest in first out (HIFO) methodology?The answer depends on the facts and circumstances.Through Q39 of the IRS’s FAQ’s for Virtual Currency, it is very clear that if the taxpayer owns multiple units of virtual currency they can choose which unit of virtual currency is deemed to be sold or exchange if the taxpayer can specifically identify which unit or units are involved.What does this allow for?Planning!Provided specific identification can take place, tax accountants can choose to create capital losses or sell certain units of virtual currency to trigger long term capital gains depending on a taxpayer’s individual income tax circumstances.

What if your client has hundreds, if not thousands, of cryptocurrency transactions?Don’t go it alone.There are a variety of tools out there that can allow taxpayers to link their wallets (which stores all their transactions) and produce the gains and losses associated with their transactions for the year.These services will even allow the taxpayer to toggle between HIFO, LIFO, and FIFO to see what gains or losses would be created under each method.Popular software in this space includes CoinTracker and Koinly.However, review still needs to be part of the process. Quirks within tracking systems could include tokens being mapped to incorrect prices and ticker symbols mapped to incorrect tokens.In addition, a review by the client is needed to ensure that outgoing transactions are truly taxable which most likely will be a conversation between to the client and tax professional to truly understand specific transactions such as staking and burning.

Another problem could occur if the digital currency was a gift or was originally purchased on a cold wallet. If a taxpayer received the currency as a gift, they are allowed to utilize the basis of the person who gifted it to them.If they transferred currency from a cold wallet, and the cold wallet is not linked to the software, the basis would be improperly recorded as the FMV of the currency on the date of transfer.The taxpayer should be reviewing these summaries.Tax professionals cannot assume they are accurate.The take-away:It is not always as easy as merely using the report issued by CoinTracker and Koinly and including the calculations on the individual income tax return.

Non-Fungible Tokens (NFT’s)

Many people became aware of NFT’s because of Christie’s auction house sale of the digital art of Mike Winkelmann for $69.3 million.The creation of NFT’s, has become a social statement and a marketing tool, with famous celebrities such as Shawn Mendes, Paris Hilton, and Eminem making millions.But what do they have to do with cryptocurrency?

NFT’s are created as part of the Ethereum blockchain and are termed non-fungible because each NFT is unique, almost like collector baseball cards.You generally are unable to purchase an NFT without owning the cryptocurrency Ethereum. While NFT’s can be copied and downloaded by anyone (yup, you can copy and download the NFT sold by Christies right now) only the person holding the NFT has the true ownership of the work.Think of the famous painting, Starry Night by Vincent Van Gogh. You may have a print of the artwork in your home, but only the Museum of Modern Art owns the original.The other benefit of the Ethereum blockchain for the creators is that a royalty fee can be established within the Smart Contract.In other words, the original creator can charge a percentage, commonly 10%, of any future sales of the digital work and it will automatically be deposited in the creator’s virtual currency “wallet” whenever any future sale occurs.Provided a creator’s digital work remains popular, the creator could have a royalty income stream for an indefinite period of time depending on the way the contract was written.

NFT’s are also being utilized in the gaming space, where a significant amount of growth is expected to occur. These so-called play-to earn games have seen a massive boom in the middle of the pandemic because of so many lockdowns.NFT’s are used as digital items inside video games, and include boxers, weapons, cosmetic skins and other in-game items owned by specific persons.Inspired by Pokémon, the Axie infinity NFT game allows players to battle, collect and build a kingdom for their pets.Players can earn additional digital currency for playing various games, breeding new monsters, and investing in land plots.One of the more popular boxing games is called Crypto Fight Club where players can fight and collect their winnings.

But what about the taxes?It is just fun and games, right? That is not what the IRS thinks, and the information that needs to be reported to the IRS is more challenging as NFT game systems generally do not keep track of all a player’s transactions.In my example above, to play Axie I would need to purchase 3 Axies, or NFT monsters, with Ethereum.This would be deemed a crypto-to-crypto transaction, which the IRS considers a taxable transaction as discussed above.

Well, that sounds easy enough. What’s the issue?That transaction just got you into the game.Now you have three NFT monsters which you will use to play the game (the equivalent of 3 Pokémon cards).When certain tasks are accomplished, you may earn SLP currency which would need to be included as income on an individual’s tax return based on the FMV on the date received.What if the player buys land in Axie Infinity with additional Ethereum?That would also be deemed as a crypto-to-crypto exchange.What if the player uses the SLP earned for playing the game to buy additional NFTs or looks to cash out their SLP to a different digital currency?Again, another taxable transaction.

Lastly, what if a player is done playing the game and wants to sell their Axies or NFTs. That again is creating another taxable transaction.The sale of NFTs, whether digital artwork or an NFT monster, is unclear.While some would jump to the conclusion that it would again trigger a long or short-term capital gain, there is a question as to whether it could be deemed a sale of a collectible.Collectibles are considered alternative investments by the IRS and include things like art, stamps & coins, cards & comics, rare items, antiques, and so on.So if the digital art is being compared to original art, and the Axie monster is being compared to a Pokemon cards, doesn’t it sound like a collectible?And the tax impact would be that the long-term capital gain maximum gain rate of 20% would increase to a collectible rate of 28%.

Is your head spinning?I am sure it is. This was a good introductory lesson to dip your toe in the water, but you most likely will have clients asking about stable coins, cold storage wallets, staking, sacrifices, DAO’s or lending and borrowing too. The one thing tax professionals can’t do is close their eyes and hope it is going away.Being from Rochester NY, it reminds me of the Kodak downfall.Kodakcreated a digital camera and invested in technology but had a difficult technology transition.Digital currency and NFT’s are not going away.It is up to advisers to start to get their head wrapped around these new inventions.If not, the tax advisor risks losing a portion of their client base, or worse, signing a tax return that they had no business signing.

This article was originally published by Lynn Mucenski Keck in Forbes on February 22, 2022.