The magical application of Section 1202 for C corporation shareholders seems too good to be true, with millions of tax dollars being saved. However, after the significant corporate tax rate reduction passed in the Tax Cuts and Jobs Act, many S corporation shareholders are wondering why they are still being excluded from this worthwhile benefit.

Section 1202 was enacted in 1993 and excludes certain percentages of gain triggered on the sale of Qualified Small Business Stock (“QSBS”) provided the stock is held for more than five years. For qualified small business stock acquired after September 27, 2010, 100% of the gain recognized upon the sale of stock can be excluded from a C corporation shareholder’s taxable income. That was not a typo! If the rules of Section 1202 apply, and the stock was acquired after 2010, a C corporation shareholder does not have to recognize gain related to the sale of their stock. The Section 1202 exclusion is limited to the greater of $10 million or 10 times the aggregated adjusted basis of the QSBS issued by the corporation and disposed of by the taxpayer.

The Congressional intent was to incentivize taxpayers to start and invest in small businesses. However, by limiting Section 1202 eligibility to C Corporations the larger entity classification population of S corporations cannot entice as many investors for start-up businesses, even though S corporations represent more small businesses across the United States. While current law allows a Section 1202 qualified small business to have a brief period as an S corporation, the lack of definition surrounding the timing and the need for start-up businesses to be flexible in their initial years does not easily avail Section 1202 benefits to S corporation shareholders.

The ability to limit 1202 to C corporations to avoid double taxation, once at the C corporation and again at the shareholder level, may have made more sense when the corporate income tax rate was 35%. However, with the significant decrease in the corporate tax rate to 21%, limiting Section 1202 to only C corporations seems to present inequity to S corporation shareholders and could potentially stunt the capability of S corporations to properly entice additional investors using the 1202 tax incentive.

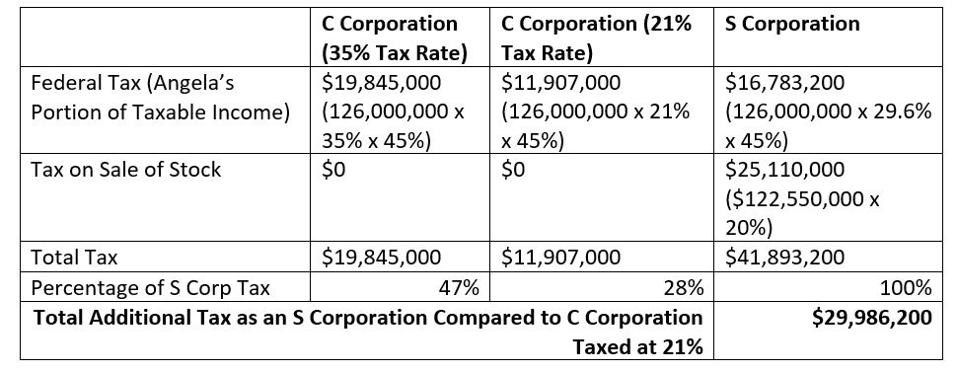

By walking through the simple example below, it is highlighted that a C corporation will only pay approximately 28% of what an S corporation would pay in the same transaction, decreased from approximately 47% when the C corporation tax rate was 35%. The C corporation shareholder can benefit not only from a reduced 21% corporate income tax rate, but the 1202 exclusion on the sale of their stock as well. Unfortunately, S corporation shareholders are still required to pay a tax rate of 29.6% (i.e., 37% less the 20% QBI deduction) on operations, plus at least a 20% tax rate on the sale of their stock.

In this example, X Company was established with the following shareholders and contributions.

C Corporation Analysis

Let’s assume that during the five-year holding period, the C corporation generates taxable income of $126,000,000 and pays federal tax payments of $26,460,000 ($126,000,000*21%). Angela decides to sell her C corporation stock after the five-year holding period when the company is valued at $450,000,000. For simplicity, no dividend distributions were made by the C corporation to Angela during the 5-year holding period.

When Angela sells her 45% interest for approximately $202,500,000 (450,000,000 x 45%), she will trigger a realized gain of $182,500,000 (202,500,000 – 20,000,000). However, provided that all the requirements of Section 1202 are met, Angela can exclude the greater of $10,000,000 or $202,500,000 (which is ten times her 20,250,000 adjusted tax basis in the QSBS sold). Therefore, none of Angela’s gain on the sale of QSBS would be taxable at the federal income tax level.

S Corporation Analysis

Applying the same example to an S corporation, the taxable income of $126,00,000 will result in federal income tax payments of $37,296,000 (126,000,000 x 29.6%). A rate of 29.6% was utilized, assuming the highest individual income tax rate of 37% less the 20% QBI deduction. As the income allocated to Angela will increase her outside tax basis, Angela’s basis will increase from $20,250,000 to $76,950,000 (20,250,000 + (45% x 126,000,000)). For simplicity, no distributions were made by the S corporation during the 5-year holding period.

When Angela sells her stock for $202,500,000, her realized and recognized gain would be $125,550,000 (202,500,000-76,950,000). Assuming a 20% long-term capital gain rate would apply to the stock sale, Angela would pay $25,110,000 (125,550,000 x 20%) in federal income taxes.

The mere utilization of a C corporation versus an S corporation would save approximately $30,000,000 in taxes related to the taxable income generated over the holding period and the sale of corporate stock.

Don’t assume that the example only reflects such a large tax discrepancy because no distributions were made during the 5-year holding period. The difference a corporate cash distribution would make would be negligible. The maximum tax rate on a C corporation qualifying dividend to an individual shareholder would be 23.8%. For the S corporation, a distribution would merely lower the basis in the shareholders stock before sale and increase the gain that is being taxed at 20%.

While it is important to advocate for S corporations to be provided the benefit of 1202, the benefit cannot apply to every corporation. Here are some highlights of the 1202 exclusion that taxpayers should be aware of.

How small does my business have to be for the stock to be deemed QSBS?

Qualified small business stock is defined as stock issued by a corporation that is a qualified small business. A qualified small business is currently defined as any domestic C corporation whose aggregated gross assets (cash, the FMV of contributed property, and adjusted basis of C corporation property) before and immediately after the issuance of stock does not exceed $50,000,000. The stock must be acquired by the shareholder at its original issue for either money, property, or as compensation for services.

Does the corporation have to be an active trade or business?

Yes. For the stock to be considered QSBS, the corporation must meet an active business requirement during substantially all of the shareholders holding period. To meet the active business requirement, at least 80% of the assets of the corporation must be used by the corporation in the active conduct of one or more qualified trades or businesses. The value of the corporation’s assets is measured for these purposes, meaning that the value of all assets, including self-created intangibles such as goodwill, should be taken into consideration in applying the 80% test.

Are certain trades or businesses excluded from the 1202 exclusion?

Yes, the following businesses are not considered qualified trade or business for purposes of 1202.

- Any trade or business involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of 1 or more of its employees

- Any banking, insurance, financing, leasing, investing, or similar business

- Any business of operating a hotel, motel, restaurant, or similar business

- The ownership of, dealing in, or renting of real property is not treated as the active conduct of a trade or business (as no more than 10% of the total value of assets can be real property that is not used in the active trade or business)

S corporation shareholders are also disadvantaged when gifting or bequeathing their S corporation stock. A C corporation that qualifies as QSBS can implement certain tax planning that would allow for the QSBS status to remain in effect for their beneficiaries (i.e., sons, daughters, and granddaughters). This would allow beneficiaries to receive the same 1202 benefits on the ultimate sale of QSBS as the person they inherited the stock from. However, the ability to pass on such a significant federal taxable income exclusion is not available for S corporation shareholders and therefore places them at an unfair advantage when looking to have a business remain in the family for generations.

As the Internal Revenue Code seems to be constantly changing, it is important for legislators to review the various incentives provided in the past to measure any new legislation’s potential impact. With a C corporation income tax rate of only 21%, it would seem unreasonable not to allow Section 1202 benefit for S corporation shareholders. Including S corporations to incentivize small businesses seems like a no-brainer. The more entities that can avail themselves to 1202 provides a higher likely hood for small business growth.

This article was originally published by Lynn Mucenski-Keck in Forbes on March 17, 2023.

Contact Us

For more information on this topic, please contact a member of Withum’s Business Tax Services Team.