On May 27, 2022, the IRS released its sixth pronouncement regarding the types of businesses that can qualify for the qualified small business stock (QSBS) exclusion.

The ruling is the fourth time the IRS has addressed the health exclusion in section 1202(e)(3), the third time it has addressed the exclusion for businesses where the principal asset is the reputation or skill of one or more of its employees, and the first time the IRS has opened the door for pharmacy businesses to qualify for the QSBS exclusion.

QSBS Generally

Section 1202 provides for the full or partial exclusion of capital gain realized on the sale of QSBS. If the requirements are met, then taxpayers can exclude from gross income capital gain in an amount equal to the greater of (i) $10 million, or (ii) an annual exclusion of 10 times their basis in the stock sold (for an exclusion amount up to $500 million). Both limitations apply on a per-issuer and per-taxpayer basis, and while the exclusion is limited to the greater of the two rules, in practice, the $10 million rule is most often the limiting factor in start-up ventures.

One important issue in determining QSBS eligibility is whether the business is a qualified trade or business (QTB). The statute defines a QTB as any trade or business other than the following excluded businesses:

- Any trade or business involving the performance of services in the fields of health, law, engineering, architecture, accounting, actuarial science, performing arts, consulting, athletics, financial services, brokerage services, or any trade or business where the principal asset of such trade or business is the reputation or skill of one or more of its employees;

- Any banking, insurance, financing, leasing, investing, or similar business;

- Any farming business (including the business of raising or harvesting trees);

- Any business involving the production or extraction of products of a character with respect to which a deduction is allowable under section 613 or 613A; and

- Any business of operating a hotel, motel, restaurant, or similar business.

For a more detailed summary of the eligibility rules relating to QSBS, read here.

The Ruling

The ruling addressed the scope of two excluded businesses: (i) the field of health and (ii) any business whose principal asset is the reputation or skill of one or more of its employees. It did not address any of the other requirements for the QSBS exclusion, such as the gross-assets test, the asset-use test, or the holding period rules.

The taxpayer in PLR 202221006 (March 3, 2022) is a pharmaceutical distributor that engages in the retail sale of a limited number of drugs. It enters into exclusive distribution agreements with the manufacturers of the drugs, but it does not manufacture any drugs itself. Its employees include licensed pharmacists that dispense drugs through the mail, and non-licensed personnel who coordinate insurance coverage with respect to prescriptions. The non-licensed personnel occasionally contact patients to inquire as to any side effects of the prescriptions and to schedule refills.

The pharmacists and other employees have no interactions with physicians other than to receive prescriptions from them. The pharmacists will interact with patients only to respond to questions, but they are not engaged in the diagnosis, treatment, or management of medical care, and interactions with patients are limited to filling and maintenance of prescriptions as ordered by a physician.

The IRS ruled that the taxpayer is not engaged in the field of health because it is not engaged in the provision of medical services to patients and its employees are not certified healthcare providers. It merely fills prescriptions and its interactions with patients are incidental to ensuring receipt of prescriptions and answering questions about the prescriptions. The IRS noted that all of the taxpayer’s revenues are generated by the sale of drugs.

The IRS also ruled favorably and without explanation that the taxpayer’s principal asset is not the reputation or skill of one or more of its employees.

The IRS concluded that the taxpayer is not in a trade or business (i) involving the performance of services in the field of health or (ii) where the principal asset of the trade or business is the reputation or skill of one or more of its employees.

Significance of the Ruling

The ruling is helpful for two reasons: (i) it builds on previous guidance that narrows the scope of the health exclusion and (ii) it confirms that the IRS will issue private letter rulings (PLRs) to taxpayers that are in the process of negotiating the sale of their businesses and not just to taxpayers with signed agreements already in hand.

This second point is particularly helpful to selling shareholders who want clarity on whether their business is a QTB so they can calculate how much tax will be due on their sale of stock. For example, if a shareholder with zero basis stock is selling such stock for $10 million, then she will pay no federal income tax if the business is a QTB and she otherwise qualifies for a QSBS exclusion. Conversely, if the business is not a QTB, then the shareholder will owe federal income tax of roughly $2,380,000 ($10 million times 23.8%).

Sellers can secure advice regarding eligibility for the QSBS exclusion either from a qualified tax advisor or from the IRS in the form of a PLR. A PLR provides greater certainty but can be more expensive to obtain because the taxpayer will have to pay the IRS user fee of $38,000 along with fees to a tax advisor to prepare and submit the ruling request, and to attend a conference with the IRS if necessary.

The IRS has discretion to issue PLRs, and ordinarily it will not issue them on alternative plans of proposed transactions or on hypothetical situations. This is where it can get tricky for taxpayers that want to obtain a PLR. Taxpayers want tax certainty in the form of a PLR before they agree to a sales price in a signed agreement, but without an agreement the IRS may not issue a ruling if it perceives the request to be hypothetical or one seeking advice on alternative plans of a proposed transaction.

It’s a classic chicken and egg situation. The IRS won’t rule on hypothetical transactions and taxpayers want tax certainty before finalizing the terms of a transaction. In the current ruling, the IRS provided a glimpse into its thinking on this issue because it issued the ruling even though it acknowledged that the taxpayer and its shareholders “are in the process of negotiating the sale of their stock . . . to an unrelated third party.” Thus, the IRS felt comfortable issuing a ruling even though no definitive sale agreement had been reached. This is welcome news to taxpayers that are considering seeking a ruling from the IRS but have not yet finalized a deal.

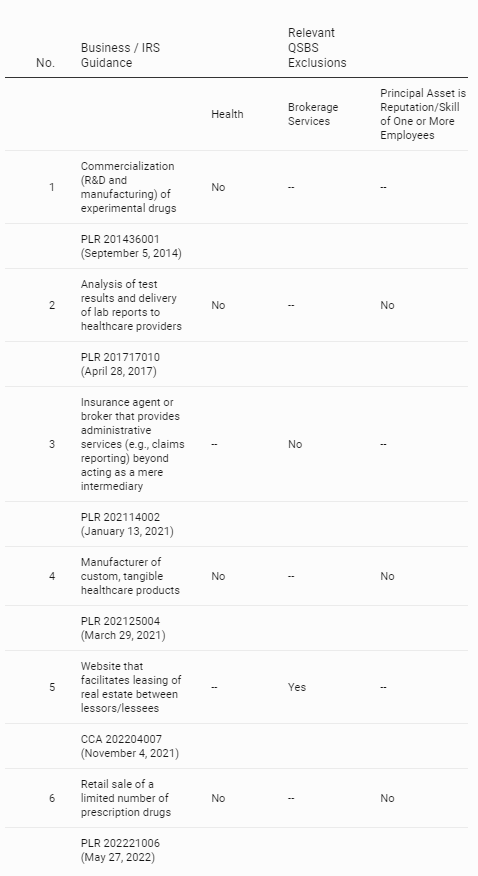

Summary Chart of Current QTB Guidance

The chart below summarizes the QTB guidance that has been issued by the IRS as of the date of this article. It includes the types of businesses discussed in the authorities and whether the IRS found the taxpayer’s business activity to be within the relevant exclusions. Recall that if a trade or business is not within an exclusion, then it is a QTB and thus eligible for an exclusion if the other QSBS requirements are met.

This article was originally published by Daniel Mayo in Forbes on June 1, 2022.