There is a lot of chatter about the $80 billion of increased funding for the IRS in the Inflation Reduction Act, which President Biden signed into law on August 16, 2022. The burning question on everyone’s mind is whether the $80 billion of increased funding for the IRS will meaningfully increase IRS audit rates. The short answer is yes, it will, but don’t expect it to happen overnight.

The IRS will have to hire and train thousands of additional revenue agents and support staff to do the work, and that is no easy task. Also, only about $46.5 billion of the headline amount has been earmarked for enforcement activity. The remainder of the funds will be used to improve operations support, to improve taxpayer services, and to modernize the IRS’s technology infrastructure, including the development of a free e-file system for individuals.

According to the 2021 IRS Data Book, the IRS in Fiscal Year 2021 had about 79,000 full-time equivalent (FTE) employees, and about 35,000 of them were dedicated to enforcement activity. Enforcement activity includes determining and collecting taxes owed, providing legal and litigation support, conducting criminal investigations, and enforcing criminal statutes related to violations of Internal Revenue laws and other financial crimes. The IRS’s total budget for FY 2021 was about $13.7 billion, with about $5 billion of such amount spent on enforcement.

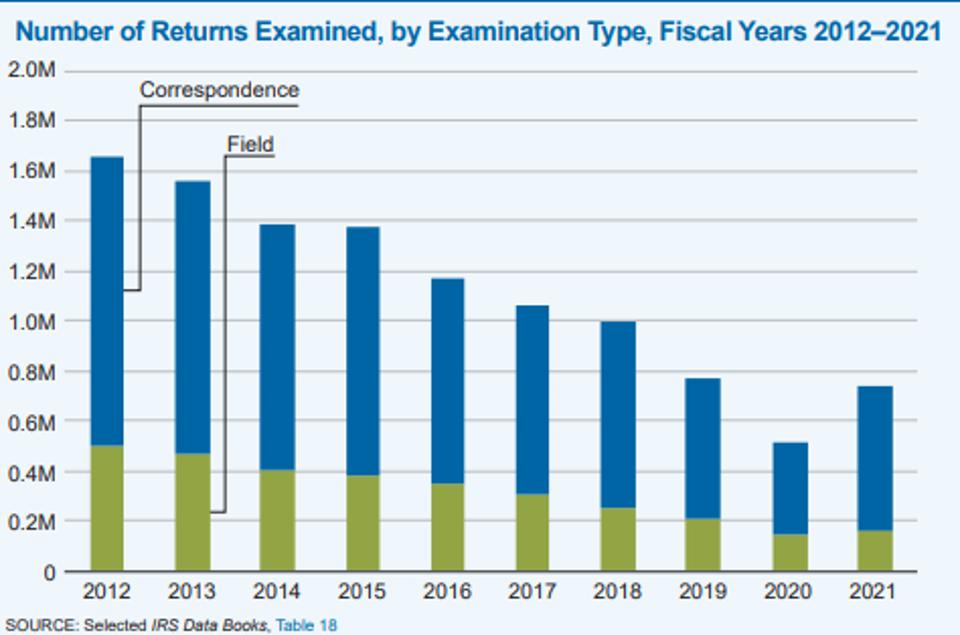

Audit rates across the board typically have been less than 1%. For years 2011 through 2019, the IRS examined 0.55% of individual tax returns and 0.92% of corporate tax returns. In FY 2021, the IRS closed about 739,000 tax examinations, and it processed more than 261 million tax returns and supplemental documents. To put this examination number in perspective, the number of tax examinations in 2021 was less than half of the number of tax examinations in 2012. The chart below shows the number of tax returns examined over a 10-year period.

Now let’s do some interesting (and very rough) math. If $46.5 billion of the increased IRS funding in the Inflation Reduction Act is earmarked for enforcement, then that translates into about $4.65 billion per year for each of the next 10 years. This would roughly double the $5 billion spent on enforcement in FY 2021. If we assume that half of the increased budget is spent to increase employee headcount (and this is just an assumption), then that would translate into an additional 17,500 FTE employees.

Let’s be generous and assume the IRS can hire 300 new enforcement employees each month (again, just an assumption) and ignore the effects of the ramp-up period and employee attrition. Under these assumptions, the IRS would be able to increase its headcount by 17,500 FTE employees in just under 5 years (17,500 employees / (300 employees/month * 12 months) = 4.86 years). Then, the IRS would have to train the new employees, and training revenue agents for high-income audits (i.e., for those making more than $400,000 per year) almost certainly would take longer than training them for less complex audits. For example, according to the IRS, a revenue agent “must be trained on the job for at least 2-3 years in order to have the experience and expertise to audit a complex return.”

If we assume that all of the increased budget is spent to increase employee headcount by 35,000 FTE employees, and use the same assumptions above, then it would take the IRS just under 10 years for it to reach its goal (35,000 employees / (300 employees/month * 12 months) = 9.72 years). And then it would still need to layer in the time it takes to train all the new employees.

With a near doubling of its enforcement budget for 10 years, the question remains whether the expected hiring spree at the IRS will translate into a doubling of the current audit rate – from less than 1% to less than 2%? Maybe, but it’s not likely to occur in the next few years, as we see in the examples above. But when the increase in audit rates does occur, it will focus on high-end noncompliance, according to proponents of the legislation. Treasury and the IRS have indicated that audit rates on businesses and individuals making more than $400,000 per year will increase at a rate faster than those making $400,000 or less.

We also expect the absolute number of audits of businesses and individuals making less than $400,000 to increase even though the percentage of such audits to the total will decrease. How do we know this? If you read carefully Secretary Yellin’s recent letter to IRS Commissioner Retting, it states that the increased funding should not be used to increase the “share” of small businesses or households below the $400,000 threshold that are audited “relative to historical levels.” This means that such taxpayers “will not see an increase in the chances that they are audited,”i.e., relative to the total number of audits. Instead, they should see a “lower likelihood of audit.”

The creative math in this article does not suggest taxpayers should start taking risky positions or expect to avoid an audit if they make $400,000 per year or less. Conversely, taxpayers making more than $400,000 per year should expect an increase in audit rates over time, but not an immediate and dramatic spike as some media reports would suggest. In sum, the gross number of audits for all taxpayers likely will increase over time, but the takeaway here is that the percentage of audits relative to the total will increase for those making more than $400,000 per year.

This article was originally published by Daniel Mayo in Forbes on August 12, 2022.