How do I classify revenue? Contribution vs. Exchange; Conditional vs. Unconditional? The Financial Accounting Standards Board (FASB) issued rules on proper not-for-profit revenue recognition criteria. For not-for-profit organizations, it’s crucial to understand how to classify these types of revenue as these changes might impact the appearance of your financial statements.

On June 21, 2018, the Financial Accounting Standards Board issued Accounting Standards Update (ASU) 2018-08, Clarifying the Scope and the Accounting Guidance for Contributions Received and Contributions Made. This ASU was issued to assist entities in evaluating whether transactions should be accounted for as contributions (nonreciprocal transactions) or as exchange transactions (reciprocal transactions) and also to help evaluate when a contribution is conditional or unconditional.

This ASU is to be applied on a modified prospective basis with retrospective application permitted. The ASU is effective for periods beginning after December 15, 2018, for entities that have conduit bond debt or periods beginning after December 15, 2019, for those that do not have conduit bond debt.

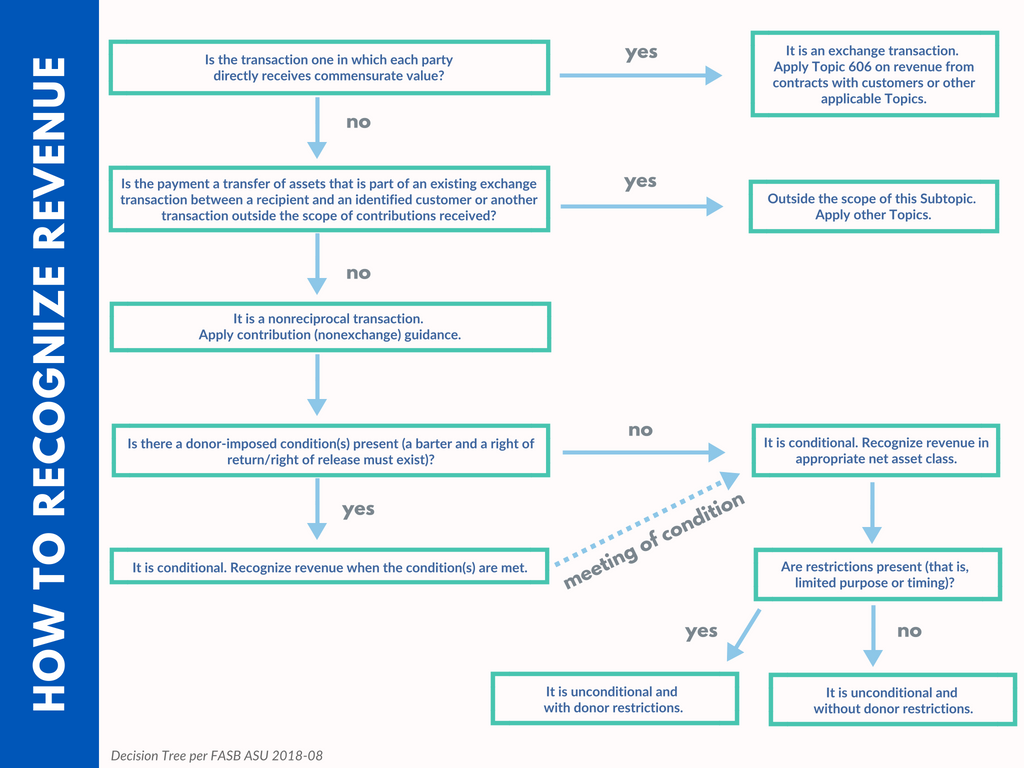

Not-for-Profit Revenue Recognition – Decision Tree

Included within this ASU are specific examples related to making the determination of whether a transaction is a contribution or an exchange transaction and also guidance to determine when a contribution is conditional. The following decision tree depicts the fives steps to follow when determining how and when to recognize revenue:

What Can You Do Now?

Understand how you recognize revenue and, in conjunction with ASC 606 implementation, start to evaluate your contracts to determine if this guidance will affect your financial statements. Generally speaking, if a transaction is an exchange transaction as determined by this guidance, you will follow FASB ASC 606. If the transaction is a contribution, you will follow the guidance in this ASU, which updates FASB ASC 958-605.

How Will The Not-for-Profit Revenue Recognition Change Affect You?

The amendments in this update likely will result in more grants and contracts being accounted for as either contributions or conditional contributions than they are under current guidance. For this reason, clarifying the guidance on whether a contribution is conditional is important because such classification affects the timing of contribution revenue and expense recognition.

If you have any questions on not-for-profit revenue recognition, please reach out to our Not-for-Profit and Education Services Group by completing the form below or contact your Withum partner.

How Can We Help?