Nearly all nonprofits offer some type of employee benefits whether tangible or intangible. Of those required benefits, organizations are sometimes unprepared for the extra resources and financial backing that the laws imply. The New Jersey commuter benefit law will find many nonprofits potentially digging for change to pay the fare.

Common Benefit Offerings

To stay competitive in today’s job market organizations offer a variety of tangible and intangible benefits. Common benefits offered are:

- Health and dental – flat amount to 100% coverage

- Retirement plan with employer match – mandatory or discretionary

- Paid time off, vacation and sick days

- Transit – varies by state, details below

New legislation in New Jersey mandates nonprofits to offer pre-tax commuter benefits to their employees.

New Jersey Commuter Benefit

New Jersey commuters will be able to use pre-tax dollars to pay for transit fees thanks to a bill Gov. Phil Murphy signed into law on March 1. Organizations will see this change impact their operations starting March 1, 2020. While this motion intends to help put money back into taxpayers’ pockets, New Jersey nonprofits will find themselves digging for change to pay the fare.

Under bill S1567, certain employers with at least 20 full-time employees must offer a pre-tax transportation fringe benefit. Employees will be able to set aside money from their paycheck, tax-free, to help offset their annual commuting costs. This model is similar to how Health Savings Accounts or Flexible Spending Accounts operate for health care costs.

2019 Commuter Transit Benefit Limits

As of January 1, 2019, the IRS allows transit commuters to set aside up to:

- $265 per month for transit passes.

- $265 per month for parking fees.

This law adds New Jersey to a list of other cities and areas with the same mandated transit benefit. Washington, D.C.; New York City; San Francisco, Bay Area counties, Berkeley and Richmond, CA; and Seattle, WA, all have a pre-tax commuter benefit program. Los Angeles, CA, may soon join the list above as it looks to pass legislation to implement a similar program.

Commuters can see up to $1,000 per year in federal income tax savings with these pre-tax deductions. Great news for individuals as they will receive tax savings from this pre-tax benefit. Not so great news for New Jersey nonprofits due to a law change in the Tax Cuts and Jobs Acts. Tax-exempt organizations in New Jersey will now be subject to Federal UBIT regulations. New Jersey nonprofits could see a 21% corporate tax rate applied to this fringe benefit offering. A massive bill to pay for many organizations that have not budgeted for this expense.

Nonprofit Transportation Fringe Benefit Tax

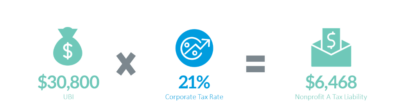

The following example shows how the New Jersey commuter benefit law will affect a nonprofit’s federal tax liability.

Nonprofit A has 27 full-time employees and must offer the New Jersey commuter benefit to all employees under the new law. 10 employees enroll in the commuter benefit plan and maximize the benefit at $265 a month for 12 months. The total pre-tax deductions taken for the year is $31,800.

Nonprofit A will claim $31,800 on its Federal Form 990-T, less the $1,000 standard deduction. $30,800 is subject to the 21% corporate tax rate.

Assuming this is Nonprofit A’s only Unrelated Business Income (UBI) source, its federal tax liability is $6,468.

Under the new law, Nonprofit A must pay $6,468 in taxes for providing this benefit to its employees.

Cost-Benefit Analysis of Employee Benefits

Organizations will need to determine how to manage this benefit best. Benefit administration will fall into the hands of third-party providers or self-management. Both of these options create an added expense for the organization – paying a third party provider or paying a full-time employee.

Nonprofits should perform a cost-benefit analysis of their employee benefits package periodically. This analysis should determine if the benefits offered are:

- Cost-effective

- Beneficial to its employees

- Competitive in the industry

Need More Guidance?

If you want to get more insight on the New Jersey commuter benefit law and how it will affect your organization or guidance on where to go from here, fill out the form below and one of our Not-for-Profit Team Members will reach out.

Authors: Brad Caruso, CPA, CFE, Partner | [email protected] and Kevin Margiatto, CPA | [email protected]

Not-For-Profit and Education Services

How Can We Help?