Will the Infrastructure Investment and Jobs Act Increase the Cost of Real Estate Construction?

Recent inflation has created a strain on real estate construction projects, as commodity and building material prices have soared. An infusion of expenditures from the Infrastructure Investment and Jobs Act (“IIJA”) is designed to spur development of the infrastructure and transportation sectors, which may create demand-side competition between real estate construction and infrastructure and transportation sectors for commodities. Here we analyze building materials common to these sectors to assess potential inflationary pressure on the demand side from the IIJA.

Inflationary Pressure on Real Estate Construction and Mining Products

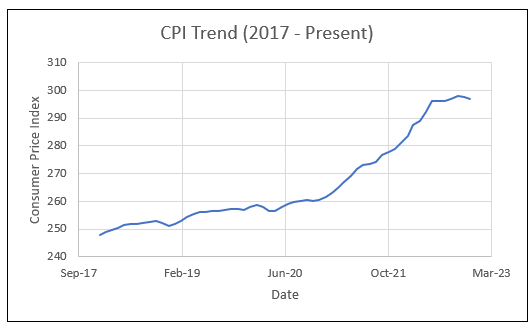

Over the last two years, inflation has placed a strain not only on households and the economy as a whole, but also on the real estate construction sector. A substantial factor in this strain is the cost of mined products used in construction and energy related to the production and transportation of such. Here we discuss only construction materials, leaving energy markets for another discussion.

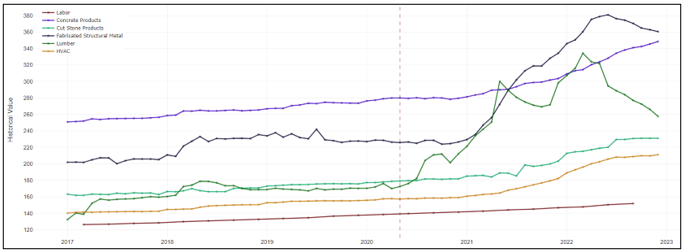

Early in the COVID pandemic, lack of demand and staffing issues due to health and travel restrictions created a temporary lag in production. This resulted in reduced supply when demand improved, while supply chain bottlenecks further impaired the flow of those goods that were available. These factors helped drive increased costs (Table 2). Simultaneously, as these supply-side constraints subside, federal legislation, such as the IIJA, pushes substantial new spending on transportation and infrastructure that, without this support, would be expected to create further stress on the supply side and act as an inflationary factor in the construction material market.

This example analyzes sand, gravel, and crushed stone. In mining terms, crushed stone is 70% limestone and dolomite. Based upon the analysis of mined product markets provided by the United States Geological Survey (“USGS”), there is substantial overlap in product usage between the real estate construction and the infrastructure and transportation sectors (Table 3). Thus, the infusion of hundreds of billions of dollars into the infrastructure and transportation sectors by the IIJA could have a substantial impact on the supply-demand balance and, therefore, the cost of construction materials.

Sand and Gravel Uses

| Construction | Industrial |

| Concrete – 50% | Hydraulic Fracturing – 64% |

| Road Base – 21% | Glass Making – 10% |

| Asphalt – 12% |

Crushed Stone

| Construction Aggregate – 72% |

| Cement/Lime Production – 24% |

The topline value of the IIJA is cited as $1.2 trillion; however, only a fraction of this is direct spending in the infrastructure and transportation sectors, with the monetary infusion extending over a decade or more. An analysis by the National Association of County Organizations projects that $550 billion in new funding will be available to all transportation and infrastructure initiatives over the next 10 years. This is a fraction of the total legislative package but still an investment of up to $55 billion per year (Table 4). Some of this funding may not be direct construction projects, e.g., a $21 billion bucket is projected for use in environmental remediation projects. Nevertheless, for the purpose of projecting the maximum potential impact of additional funding, we use the top line number of $550 billion.

IIJA Funding Projection

| Investment Allocation | Funding ($BUSD) |

| Transportation | $284 |

| Water | $55 |

| Broadband | $65 |

| Energy and Power | $73 |

| Environmental Remediation | $21 |

| Western Water Infrastructure | $8.30 |

| Resiliency | $46 |

The next question is, how much do we typically spend on transportation and infrastructure? A 2019 Brookings Institute analysis of Congressional Budget Office data suggests that this spending has trended downward since 2007 with a range of roughly $430 – $470 billion per year (Shifting into an era of repair: US infrastructure spending trends; Brookings Institute, 2019). Another important finding of this report is that spending has trended away from capital programs and toward repair and refurbishment of existing infrastructure, what the Brooking’s Institute refers to as the “Era of Repair.”

While repair projects are expected to remain dominant, there are a number of positive developments and infrastructure expansions that are known to have already benefitted from IIJA funding, such as airport and seaport expansions and, notably, the long-dormant I-86 expansion project in New York, which has been added to the New York State Department of Transportation’s 5-Year Capital Plan with at least $1 billion in new funding, partially from the IIJA infusion.

Based upon the capital infusion projections, the maximum demand increase as a result of the IIJA is 12% ($55 billion new funding vs. $450 average spending). And indeed, many commentators have speculated that this infusion will result in a boom in demand for infrastructure construction materials and an increase in activity within the eminent domain and condemnation space to facilitate new development[1].

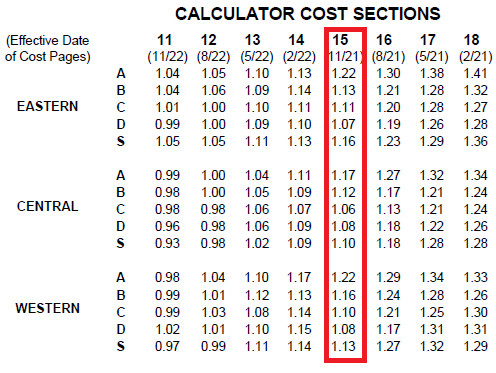

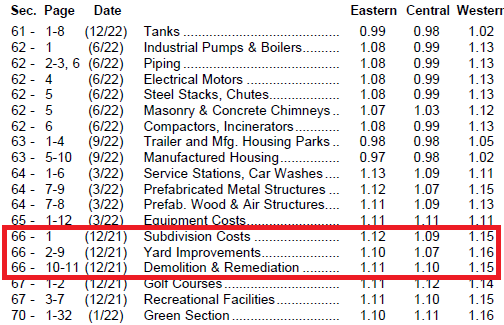

But does the new spending offset recent inflation? The IIJA was signed into law in November 2021. Thus, several inflation indicators are reviewed to see how the construction materials market has changed its implementation. The first indicator is the Marshall & Swift Valuation Services Cost Manual (Table 6). General real estate construction cost is presented, followed by Subdivision & Yard Costs, which include cost of roadways. The effective dates of these are December 2022. Many construction classes have already experienced inflation of 12% or greater since the IIJA passed.

More specific to the infrastructure and transportation sectors, the Federal Highway Administration publishes the National Highway Construction Cost Index on a quarterly basis. As noted in Table 7, from 4Q2021 to 2Q2022, two quarters post-IIJA, the index increased 17% from 2.18 to 2.55. Consequently, the cost of construction has already outpaced all new spending projected from the IIJA.

Overall, the data suggests that additional funding provided to transportation and infrastructure projects over the next decade is unlikely to offset inflation and, therefore, should not create a demand-side driver of future inflation or increased competition with real estate construction programs for construction and mined products.

Economic conditions and energy prices play a large role in construction costs, with falling commodity prices being a leading indicator of recession. With speculation about an impending recession (or soft landing) and the observation that energy prices are falling (oil has fallen from a high of $147/barrel in June 2022 with a projection of $77/barrel in 2024 per the US Energy Information Administration), construction material cost are expected to stabilize in the next two years.

[1] Excerpts from Valuation Magazine, Q2 2022, “Infrastructure in Favor,” The Appraisal Institute, Chicago.