As the Financial Times reported on April 2, the U.S. Treasury is urging regulators to convene now on the risks building in private credit—an indication that concerns around governance gaps in the sector are beginning to intensify.

Recent redemption constraints weren’t a sign of failure in private credit, but they did bring a long-standing tension into sharper focus. Semi-liquid structures offer periodic liquidity, yet they’re built on portfolios of inherently illiquid, long-duration loans. That model works smoothly when confidence is strong and pricing remains stable. But as interest rates rise, spreads widen, and refinancing assumptions come under pressure, that balance becomes increasingly delicate.

In this environment, net asset value is no longer a passive reporting outcome. It is an economic signal. How funds value, stress, and communicate their portfolios now plays a central role in whether investor confidence holds — or liquidity evaporates.

For years, semi-liquid private debt vehicles worked because confidence was high, refinancing was easy, and spreads were tight. NAVs were stable. Redemptions were manageable. “Performing equals par” was rarely questioned.

That environment has changed.

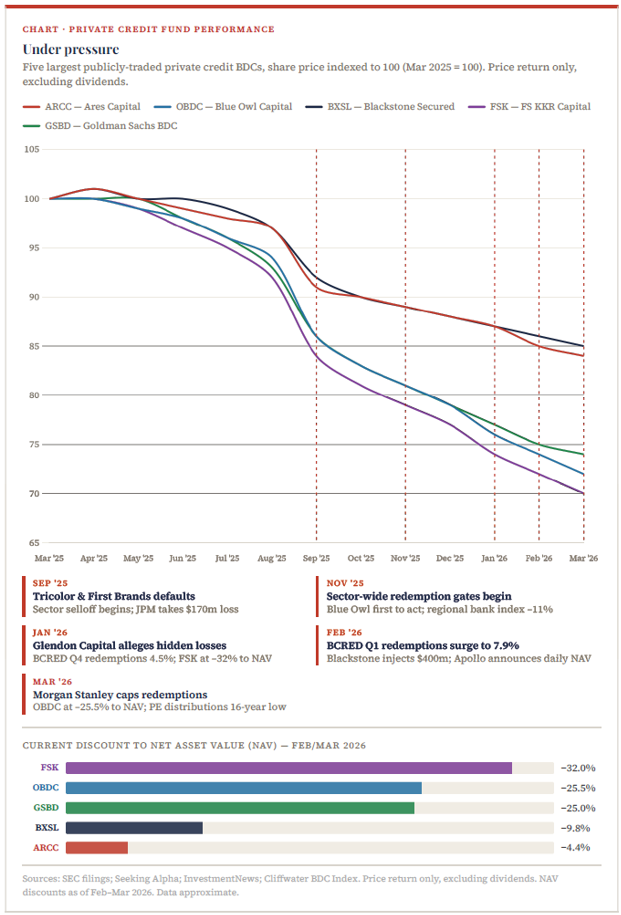

Higher rates, widening refinancing walls, and idiosyncratic defaults — Tricolor Auto and First Brands Group — have cast doubt. When doubt enters, redemptions follow. When redemptions follow, gates close. And when gates close, the discount widens regardless of whether the underlying loans are impaired.

Redemptions are rarely triggered solely by losses. They are triggered by doubt.

The Key Distinction

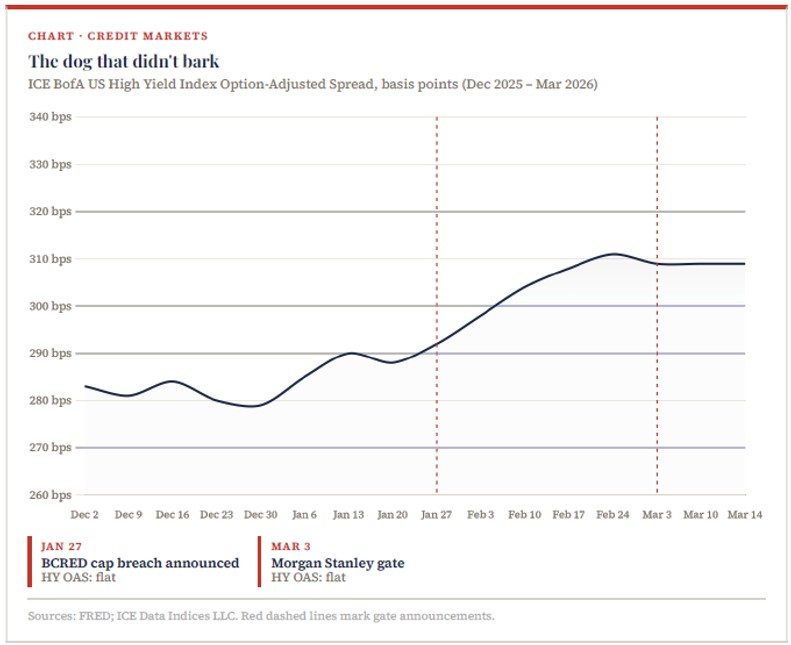

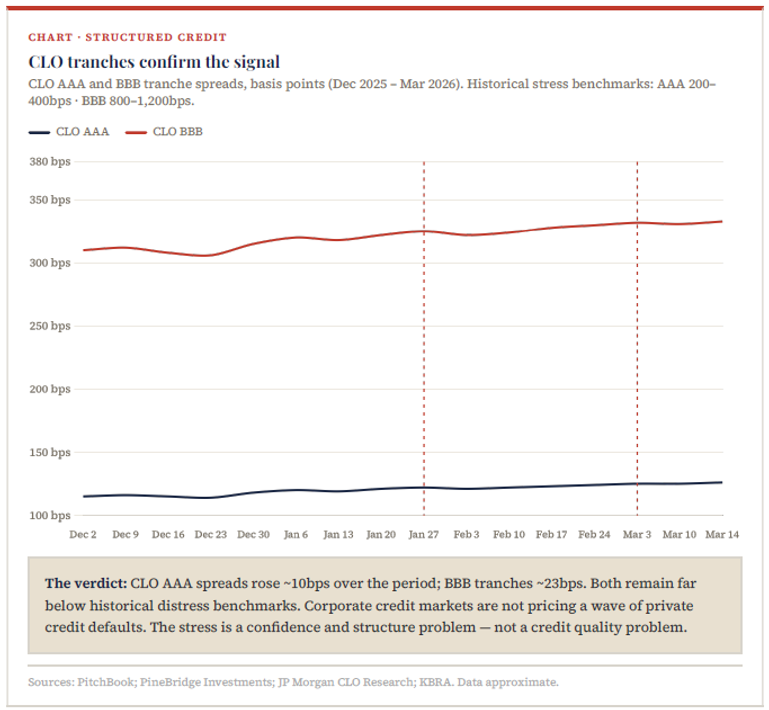

This is not a credit crisis. It is a confidence crisis.

The evidence lies in markets that reprice in real time. If the BDC selloff reflected genuine corporate credit fear, it would appear in high-yield spreads. The ICE BofA US High Yield OAS closed March 2026 near 309 basis points — essentially unmoved since the redemption wave began in November 2025.

Implications

The gap between public price and private NAV is the crisis.

FSK trades at a 32% discount to its stated NAV. OBDC at 25.5%. In a semi-liquid structure, NAV is not just an accounting output—it is the exit price. When investors believe marks are stale, they submit redemption requests today — rationally, defensively — before marks adjust tomorrow. Apollo’s announcement of daily NAV marking is the industry’s clearest acknowledgement that the gap between economic reality and reported marks is the problem. The answer, in every case, is to look harder at the underlying assets.

The next phase of private credit will be defined less by yield and more by credibility.

Recommendations for Funds Under Pressure

Three practices that build investor confidence — and help keep gates closed.

Recommendation 01: Dynamic Portfolio Valuation

- Recalibrate marks continuously against public market signals.

- Quarterly valuation cycles anchored in prior assumptions are no longer sufficient in a market that reprices daily. Funds should move toward continuous discount rate calibration tied to observable inputs. Benchmark discount rates weekly against leveraged loan spreads, CLO pricing, and HY OAS — not quarterly against internal estimates.

- Model refinancing risk explicitly: a loan maturing in 18 months in a spread-widening environment is not worth par.

- Decompose NAV into performance value and liquidity premium, so investors can see what portion requires a liquid exit to realize.

- Adopt gradual repricing protocols. Sudden step-downs in a single period destroy trust faster than the write-down itself.

Recommendation 02: Forward-Looking Portfolio Monitoring

Replace backward-looking reports with scenario-based foresight.

Most reporting explains what has already happened. Investor confidence depends on understanding what is likely to happen next.

- Publish borrower-level EBITDA stress tests with base, downside, and severe scenarios updated quarterly.

- Build and publish a refinancing wall dashboard: maturities in 12–24 months, leverage, and estimated refinancing spread delta.

- Track and disclose PIK loan concentrations as a leading indicator of stress before it manifests in write-downs.

- Benchmark borrower performance against origination underwriting every quarter.

Recommendation 03: Valuation Governance

Eliminate the perception of manager bias through independent oversight.

Allegations such as those raised by Glendon Capital — regardless of their ultimate accuracy — signal a broader issue: trust in manager-determined marks has weakened. Governance is the structural response.

- Establish a Valuation Committee with independent members holding final authority over Level 3 marks; publish methodology quarterly.

- Engage external valuation specialists for ≥25% of portfolio by value each quarter, rotating for annual full-book review.

- Disclose discount rates by industry bucket and their quarter-over-quarter movement.

- Commit publicly: if redemption pressure exceeds a stated threshold, an independent third-party review will be commissioned.

Private credit is not broken. But the era of “liquid illiquidity” demands tighter alignment between economic reality and reported marks.

In semi-liquid structures, NAV is not just an accounting output. It is the exit price. If investors trust it, liquidity holds. If they don’t, gates follow.

Author: Farrukh Alimov, Team Lead, Portfolio Valuation and Fund Advisory Services | [email protected]

Contact Us

For more information on this topic, please contact a member of Withum’s Forensic and Valuation Services Team.