The Elephant in the Not-For-Profit Boardroom

How to Bring Your Development and Finance Teams Together in Harmony

Nonprofit finance and development teams each bring a unique perspective to an organization’s finances: not right, not wrong, but certainly different. Fundraising professionals focus on successfully raising money, while CFOs narrow in on compliance rules to account for it. Such fundraising strategies and accounting regulations can lead to mismatched reports even with tight operations in place. Disparate numbers erode stakeholder confidence and can threaten an organization’s long-term sustainability and impact.

Chapter 1: The Elephant in the Not-For-Profit Boardroom

It’s the first board meeting of the quarter and the development director has just completed her 2015 board report. She’s thrilled to announce that in the past year—through a combination of major donor contributions and grants—the Fundraising team has raised over $5 million, exceeding their target by $250,000. Amazing! Well done! A fabulous year. She receives a round of applause from the room and walks back to her seat with a glow.

But then a troubled look from a new board member breaks the mood: “I’m looking at the Statement of Activities and it shows $4 million dollars in contributions for 2015. That’s a pretty big difference. What’s going on? What number is correct here? A million- dollar difference is a pretty big deal.”

All eyes are on the report, and the development director jumps in to explain that she received a confirmed pledge from a major donor that should have been counted. The CFO responds that the pledge itself can’t be counted because in all reality, it wasn’t a pledge, it was a conditional gift—the donor pledged $750,000 to the capital campaign but only under the condition that the proposed building site go through an environmental impact report. “What? I’ve had multiple conversations with the donor and we both know that’s a formality!” Conversational mayhem ensues until the Executive Director steps in and promises to get a set of clarifying numbers within the week.

Three months later the Executive Director has been replaced by an interim (the current chair of the Finance Committee) and they now have an executive search firm looking for a leader with a strong finance background.

Reporting Meltdown: What Happened?

Was the Development Director overpromising? Or was the CFO a nitpicker underestimating dollars raised? No and no. The perspectives of the Development Director and the CFO reflect the ancient parable of a group of blind men who touch an elephant to understand what it looks like. Each individual traces just one body part and describes the elephant based on what they’ve touched: the man who feels the leg says the elephant is solid, like a pillar or the trunk of a tree; the man who handles the tail says the elephant is slender and bendable, like a rope. As each man truthfully describes the elephant, they find themselves in utter disagreement, defending their own positions and questioning the experience of the other men.

Finance and Development each bring a unique perspective to an organization’s finances: not right, not wrong, but certainly different. And the numbers won’t necessarily match up even with tight operations in place.

Why? Because neither is reporting on the whole of the elephant, instead they are reporting on the elephant’s trunk or its tail.

The Root Cause: Fundraising Strategies vs. Accounting Regulations (GAAP and FASB)

The CFO lives in a world of compliance and audits guided by Generally Accepted Accounting Principles (GAAP), an accounting industry framework that defines how money should be properly accounted for, spent and reported upon.

For nonprofits, the GAAP Statement of Financial Account Standards (FASB 116 and 117) introduces specific accounting rules that stipulate how gifts should be recorded and reported upon. Under FASB 116, all contribution revenue must be classified as either unrestricted; temporarily restricted; or permanently restricted. FASB 117 is a supporting rule that determines how contributions need to be reported upon.

And here the parable of the Elephant begins. FASB rules present accounting and reporting constraints that are often foreign concepts to a Fundraising professional.

The Development Director is interested in the most successful ways to raise money for the organization and how much money has been raised. Their world is a world of relationships.

A fundraiser is tasked with raising money for both the general operating fund as well as specific programs, and so keeps a keen eye on donor intent so as to know when to ask whom for what. A primary metric is reporting on how contributions have been generated and the relative effectiveness of those strategies. Terminology such as “campaign” and “appeal” and “fund” are used to describe fundraising initiatives and what program they’re raising money for.

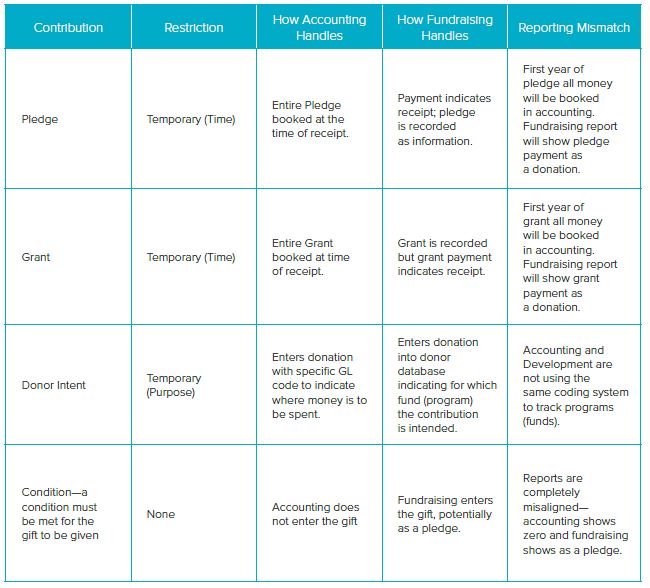

Two common development strategies are pledges, where a donor pledges to pay a certain amount of money over time; and grants from private, corporate and governmental organizations.

FASB 116 essentially puts constraints upon the recording of pledges, grants and those gifts a donor intends for a specific program. Accounting must abide by FASB 116 regulations, which require that a pledge is recorded in its entirety at the time of the pledge. A similar logic is used for grants.

None of these restrictions exist for a fundraiser. And this is a primary reason that fundraising and accounting reports don’t align.

For example, if a donor pledges $50,000 with the intent to pay $25,000 in four quarterly installments for one year, the fundraiser will record a pledge as $50,000 as a “placeholder” but will record each pledge payment as a donation of $12,500 when the check is received. Monthly and yearly donation reports will include the pledge payments received to date, not the pledge. A separate report is run for pledges and pledge payments against the pledge.

Accounting on the other hand, will record the pledge in its entirety at the time that the pledge has been made. So their contribution report will show $50,000 immediately.

Since Fundraising and Accounting often use different databases, the reports will reflect the elephant’s trunk or its tail, leaving executive leadership confused about the financial status of their organization.

Restrictions in a Nutshell

All contributions to an organization fall into three buckets: temporarily restricted, unrestricted and permanently restricted.

Bucket 1: Temporarily restricted contributions are:

- Purpose-restricted: The donor requests that the money be used for a specific program or purpose.

- Time-restricted: These contributions are sometimes referred to as multi-year gifts because the gift that will be given over a period of time. Examples are pledges and grants. The amount to be received in future years is considered time-restricted.

Bucket 2: Unrestricted support consists of all other revenue without donor constraints. A donor just sends in a check.

Bucket 3: Permanently restricted support is most commonly an endowment fund. Generally, the principal cannot be used but the organization can use investment earnings. The earnings on permanently restricted funds may be further restricted for a specific purpose, then becoming temporarily restricted revenue.

Conditional gifts, though technically, not a restriction, will affect accounting and reporting. Conditional gifts are gifts that must meet a requirement for a donor to give. A common example is a matching requirement. A donor will give $25,000 to an organization if the fundraiser can raise an equal amount.

Timing Issues

Last, there is an accounting process called “release from restriction,” a process by which restricted monies are released into the unrestricted “bucket” when a condition has been met, for example when a program expense occurs. An accounting procedure moves that money into the unrestricted bucket so it can be spent. The Balance Sheet and the Statement of Activities (Income Statement) are two financial reports that can confuse readers—particularly fundraisers—because they categorize both restrictions and the movement of money into different buckets, so as money shifts from bucket to bucket the numbers can look very different than dollars raised on a basic fundraising report.

Common Mismatches

Chapter 2: How to See the Whole Elephant in the Boardroom

Education

Not everyone is an accountant, nor do they wish to play one on TV or in the boardroom. Yet board and executive leadership have a fiduciary responsibility to their organizations. Understanding nonprofit accounting rules and how to read financial statements is a critical factor in stewardship. Educating Fundraising and Board leadership on accounting regulations can be accomplished through sector resources such as Boardsource, the Nonprofits Assistance Fund and the Nonprofit Finance Fund. Even a cheat sheet of terms can be helpful for fundraisers to understand how the accounting department is viewing dollars raised.

Conversely, Fundraisers can educate Finance as to the campaign and appeal strategies that help them build relationships and revenue. Fundraising software has standardized reports that development officers may assume that others understand, such as LYBUNT (donors who gave last year but not this year), and these reports give another angle on the financial health of an organization.

Operations

This is the belly of the beast. Apart from the organic differences introduced by FASB accounting rules, there are a handful of day-to-day operational checkpoints that if missed, will introduce differences in reporting that in effect, are mistakes.

- Chart of Accounts

The Chart of Accounts is the primary organizing tool for getting money put in the right buckets. Fundraising software uses the term “fund” which is where money is being designated such as a specific program. An accounting software may refer to “fund” as the restriction type. For reports to line up, both Fundraising and Finance need to be using the same Chart of Accounts structure for the fund designation. This may seem obvious, but in many cases it isn’t. Aligning the Chart of Account is an ongoing process because programs come and go, software comes and goes, and people within the organization come and go.

- Gift Entry and Monthly Reconciliation

The gift entry process is the heart and soul of nonprofit operations. Assuming here that development enters gifts into their fundraising database and accounting enters information into their accounting software, double entry occurs. For reports to match, it’s critical that a system is put in place

to reconcile gifts between both software solutions. For this purpose, a “batch” system is recommended where gifts are entered individually by the Fundraising team using the shared chart of accounts code for the fund (designation or program). At the end of the data entry, a batch report is exported from the fundraising software with the batch number and total gift amount, organized by the chart of account code. The accounting system will use the batch number and chart of account code to create a journal entry for the gift amount total. Special attention must be made to pledges, pledge payments, grants, grant payments and stock gifts as they have specialized accounting rules constraining their entry.

Using this method, reconciliation between systems can be done on a daily, weekly or monthly basis, which will identify errors and maintain the data hygiene needed for accurate reporting.

Collaborative Reporting

When the Fundraising and Finance teams are aligned on data entry operations,

they can build reports that play on each other’s strengths rather than weaknesses. Fundraising software is designed to create summaries of campaign strategies, top donor reports and an overall picture of strategy strengths. The goal in fundraising reporting is to build confidence in the initiatives being used to generate funds and the potential contributions in the pipeline.

The Finance team understands accounting rules and is in the best position to explain how accounting rules will affect numbers reported by Finance versus Fundraising. In specific, by collaborating ahead of time on how temporarily restricted contributions such as pledges and grants will be reported upon, with prepared notes explaining differences, the board and executive leadership will leave the meeting with a clear picture of the organization’s financial health.

Remember the parable of the blind men and the elephant: Finance and Fundraising are describing two different parts of the elephant. Give the Fundraiser the “glory of the donor story” and leave the detailed accounting explanations to Finance.

Chapter 3: Is Technology Integration the Final Frontier?

Maybe. But only if the business processes are carefully orchestrated between Fundraising and Finance, so that the unique needs of both departments are understood and met. Fundraising and Finance do have a meet and greet at the transaction; but fundraising connects the transaction to an organization, a household, or an individual—and further—needs to track and report on marketing data associated with the transaction. Accounting has no such need and manages the transaction from both a revenue and expense perspective. Fundraising knows and cares little about expenses, they just want to make sure that their campaigns for programs are well funded.

Integration between a fundraising software and an accounting package is often thought of as a holy grail, with the goal of one-and-done data entry and reports that would satisfy everyone at the boardroom table. But to get to this Promised Land, three things are needed:

-

Data Mapping and Business Process Design

Finance and Fundraising must first be able to roll up their sleeves at the data and operational level, synchronizing coding structures and mapping multiple criteria to a transaction. Assuming that both a fundraising technology and an accounting solution will be used, hard choices will need to be made about which solution will be used for specific business processes. Development and Finance will need to talk through a lot of operational detail potentially changing how things are done in the day-to-day. Since most of us don’t like change, particularly when big-ticket items are involved, expect the boat to rock while sailing to the Promised Land.

-

Appropriate Technology

At least one of the technologies will need to have the ability to be customized to accommodate additional data and business processes. Internet solutions such as Salesforce.com and Netsuite are “development platforms” that provide the ability to customize, script and integrate data from external sources using web services. The choice of an ERP (Enterprise Resource Platform) such as Netsuite allows an organization to use a system of integrated solutions to automate many back-office functions, going beyond siloes of fundraising software and accounting.

-

Vision

Nonprofits are living in a new era, where donors see themselves as investors looking for proof of an organization’s effectiveness before they contribute. Nonprofits in a sense are pushing back on what constitutes effectiveness, debunking the notion that laurels should be given to organizations with the smallest percentage of administrative and fundraising overhead. The Overhead Myth, a letter from the CEOs of Guidestar, Charity Navigator, and Wise Giving Alliance has broken new ground by publicly busting the myth of the overhead metric. The letter encourages not-for-profit leaders to share reports about the true costs of achieving their missions so that funders and nonprofits can do a better job of resourcing their programs. Technology used to integrate systems needs a bigger picture than just linking fundraising and finance.

To return to the analogy of describing the entire elephant, technology can certainly support better tracking of data and thus better reporting. But technology alone is not the answer. A vision of transparency, impact, and stewardship of resources is a choice that your board and executive leadership must first make. Ask yourself: What’s most meaningful about the work that we do and how will we track and communicate stewardship and progress toward our goal? Replace fractured thinking between fundraising, program and finance, and use technology to capture the information needed to accurately communicate where you stand. Up your game and stop using the same tired functional expense pie-charts to demonstrate effectiveness. Financial ratios are not your core accomplishment, fundraising is not your mission, and technology is not the point. The point is how many meals were delivered to seniors, how many pets got adopted, and how many trees got planted. What resources were needed to accomplish these goals? How will you sustain these programs into the future? Reports that monitor, enlighten, steward and strategize are the reports your donors, board, and leadership want to see. Take the lead, and use technology to track and communicate a picture of the whole elephant, not just the trunk or the tail.

Please contact a member of Withum’s Cloud Solutions and Management Consulting Services team, fill in the form below.

Disclaimer: NetSuite and the NetSuite logo are service marks of NetSuite Inc. Third-party trademarks mentioned are the property of their respective owners. The use of the word partner does not imply a partnership relationship between NetSuite and any other company.

How Can We Help?